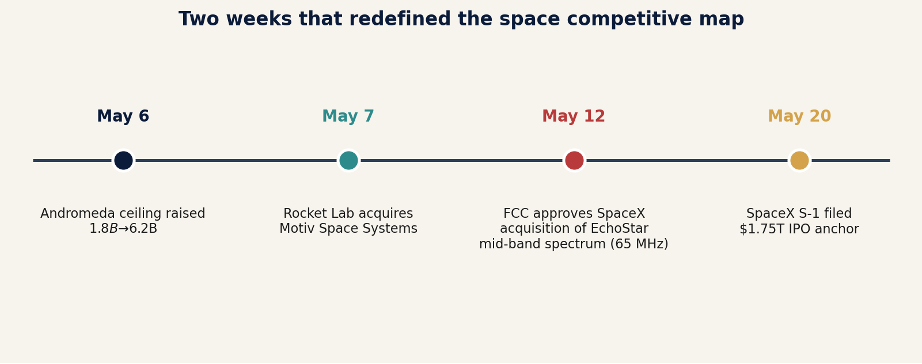

Two Weeks That Redefined Space

SpaceX walked into Wall Street as a telco-AI conglomerate. The Pentagon tripled its bet on watching GEO. The competitive map looks nothing like it did a month ago.

Four announcements in fifteen days — and a structural shift underneath all of them.

If you blinked between May 6 and May 20, you missed two of the most consequential signals the space industry has produced in a decade. One came from a public S-1 filing. The other came from a quietly raised contract ceiling. Together, they tell you everything about where this business is going.

The commercial side just declared that launch is no longer the main event. The national security side just admitted that the architecture it built to watch the high frontier is no longer adequate. Neither of those statements would have been made out loud last year. Both are now on the record.

Here is what the two moves mean — separately, and together.

Part One — The SpaceX IPO Isn’t About Rockets

On Tuesday morning, May 20, SpaceX dropped the most consequential document the space industry has ever read: its public S-1. Wall Street saw a $1.75 trillion valuation chasing the largest IPO in history. The rest of us got something more interesting — a 400-page admission that SpaceX no longer thinks of itself as a space company. And once you accept that, the competitive map of this industry looks completely different than it did last Friday.

The numbers that reframed the conversation

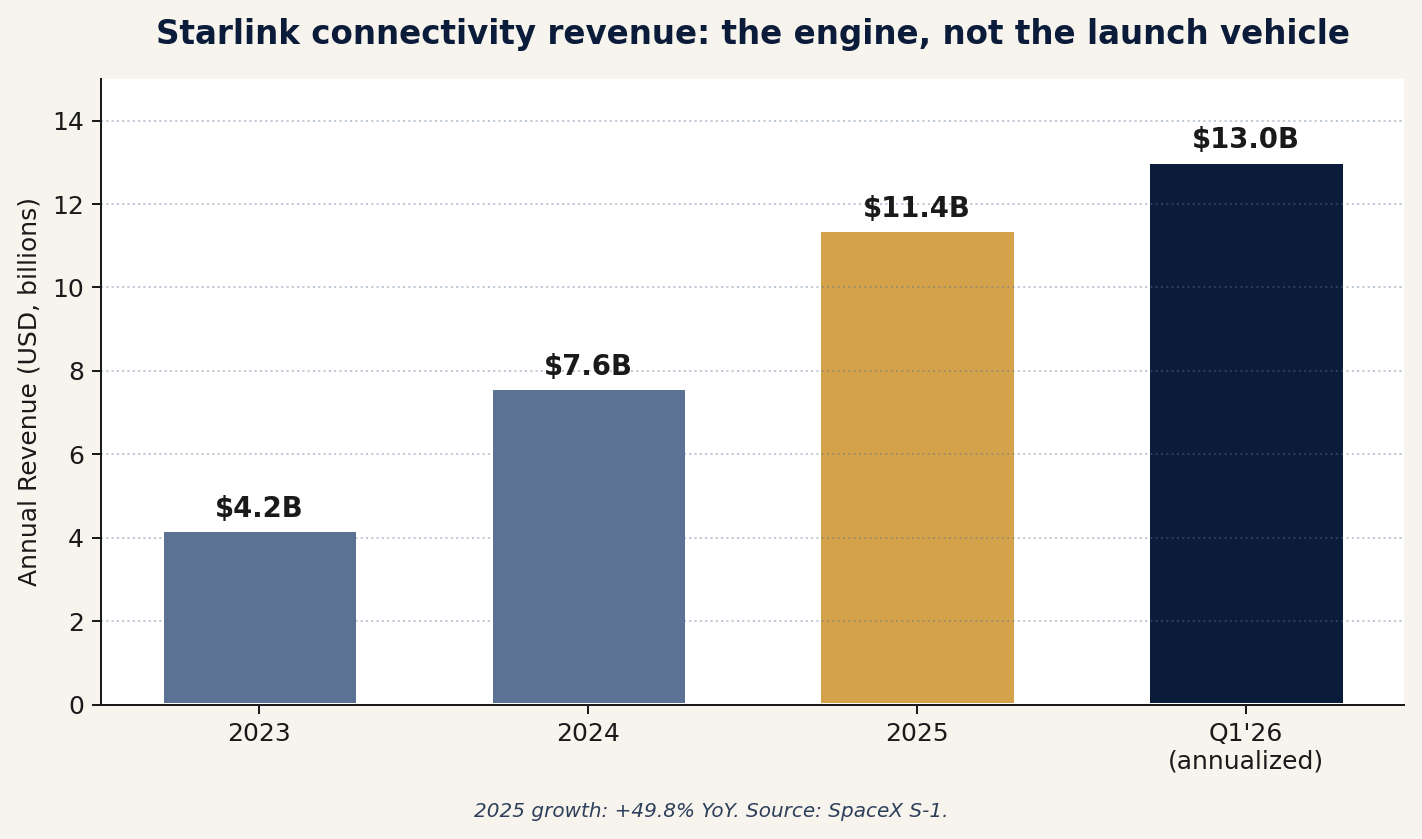

Start with what the filing actually says. Starlink’s connectivity segment generated $11.4 billion in revenue in 2025, up 49.8% year over year, and another $3.26 billion in Q1 2026 alone. Launch — the business that built the company, terrified the primes, and reshaped global access to orbit — is now a supporting act.

Starlink connectivity has gone from a curiosity to the dominant revenue line in five years.

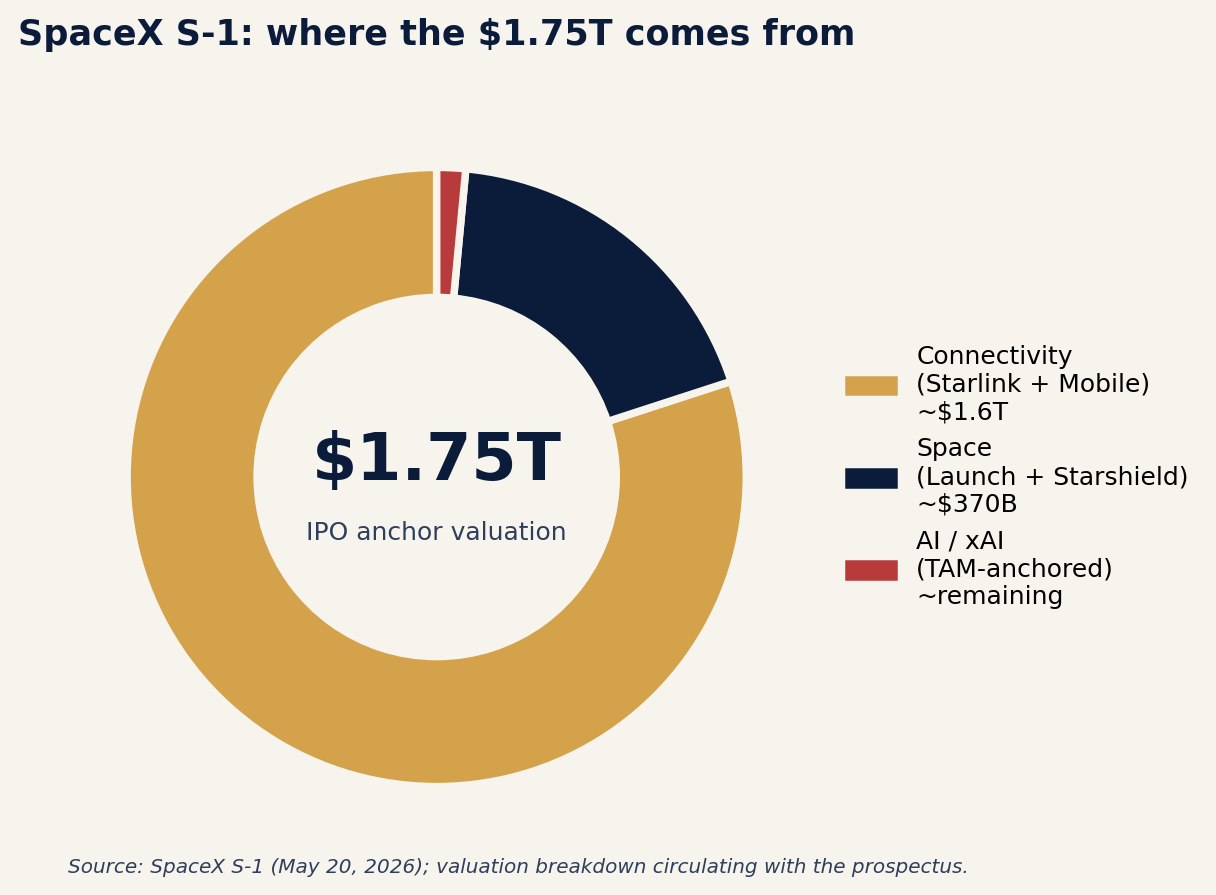

In the valuation breakdown circulating with the prospectus, “Space” carries roughly $370 billion of the $1.75 trillion price tag. “Connectivity” carries about $1.6 trillion. And a third bucket — AI, anchored by the February merger with xAI — is being marketed against a $26.5 trillion total addressable market.

SpaceX is asking public investors to buy a launch company and pay nine-tenths of the price for everything else.

That ratio is the story.

The telco inside the rocket company

Read closely, the prospectus is a declaration of war on the wireless industry. SpaceX is pitching Starlink Mobile as a $740 billion addressable market — within shouting distance of its $870 billion broadband TAM — and explicitly says next-generation direct-to-smartphone service will be “on par with terrestrial mobile networks” in urban areas, not just a remote-area backup.

The technical foundation arrived eight days before the filing, on May 12, when the FCC approved SpaceX’s acquisition of 65 MHz of contiguous mid-band spectrum from EchoStar. That spectrum, combined with the V3 satellites Starship just started flying, is the package needed to push real 5G — SpaceX is targeting 150 Mbps — directly to off-the-shelf phones by late 2027.

If that capability lands anywhere close to spec, the implications cascade hard. Verizon, AT&T, and T-Mobile suddenly compete with a constellation that doesn’t need to lease tower real estate or trench fiber. Rural carriers face an existential question. International telcos that were planning to partner with Starlink will reassess whether they’re partners or prey. The MNO-MVNO model that has structured global wireless for thirty years gets reframed as a distribution channel.

Musk bought an AI company with SpaceX’s balance sheet

The other surprise in the S-1 is how deeply xAI is now woven into the business. The February all-stock merger valued the rocket maker at $1 trillion and the chatbot maker at $250 billion. In Q1 2026, the AI unit lost $2.47 billion on $818 million of revenue — most of the spending came from training infrastructure at the Colossus and Colossus II data centers in Memphis. It is also where the cash is coming from: Anthropic is contracted to pay $1.25 billion per month for compute through May 2029, a deal that is now SpaceX’s largest non-Starlink revenue line.

That changes the analytical frame for everyone in our industry. SpaceX is the only space prime whose public investors are also buying exposure to frontier AI training compute and a contracted relationship with one of the two leading model developers. None of the heritage primes can match that pitch — and neither can any other launch competitor.

Underneath all of it sits a dual-class share structure that gives Musk 85.1% of the voting power post-IPO. Public investors get the upside; he keeps the steering wheel.

What this does to the rest of us

If you build, fund, or buy from space companies, the IPO changes your operating environment in three concrete ways.

Capital gravity shifts hard. A successful $75 billion raise pulls institutional money toward SpaceX’s orbit and away from second-tier launch and constellation plays. Rocket Lab, Relativity, and the European launch entrants will have to argue their differentiation against a public comparable that just printed the largest market cap in space history.

The “build it or buy it” math changes for primes. Lockheed, Northrop, Boeing, L3Harris, and RTX have spent two years adjusting to a SpaceX that competes on launch. They now compete with a SpaceX that competes on launch, on broadband, on direct-to-cell, on AI compute, and on classified national security constellations (Starshield), with a $1.75 trillion balance sheet and a CEO who answers to himself.

Regulatory posture hardens. Once SpaceX is a public company, every spectrum proceeding, every export-control change, every counterspace policy question carries shareholder consequences. The lobbying intensity ratchets up. The FCC, FAA, and Commerce face a counterparty with a fiduciary mandate to push.

Part Two — The Pentagon Just Tripled Its Bet on Watching GEO

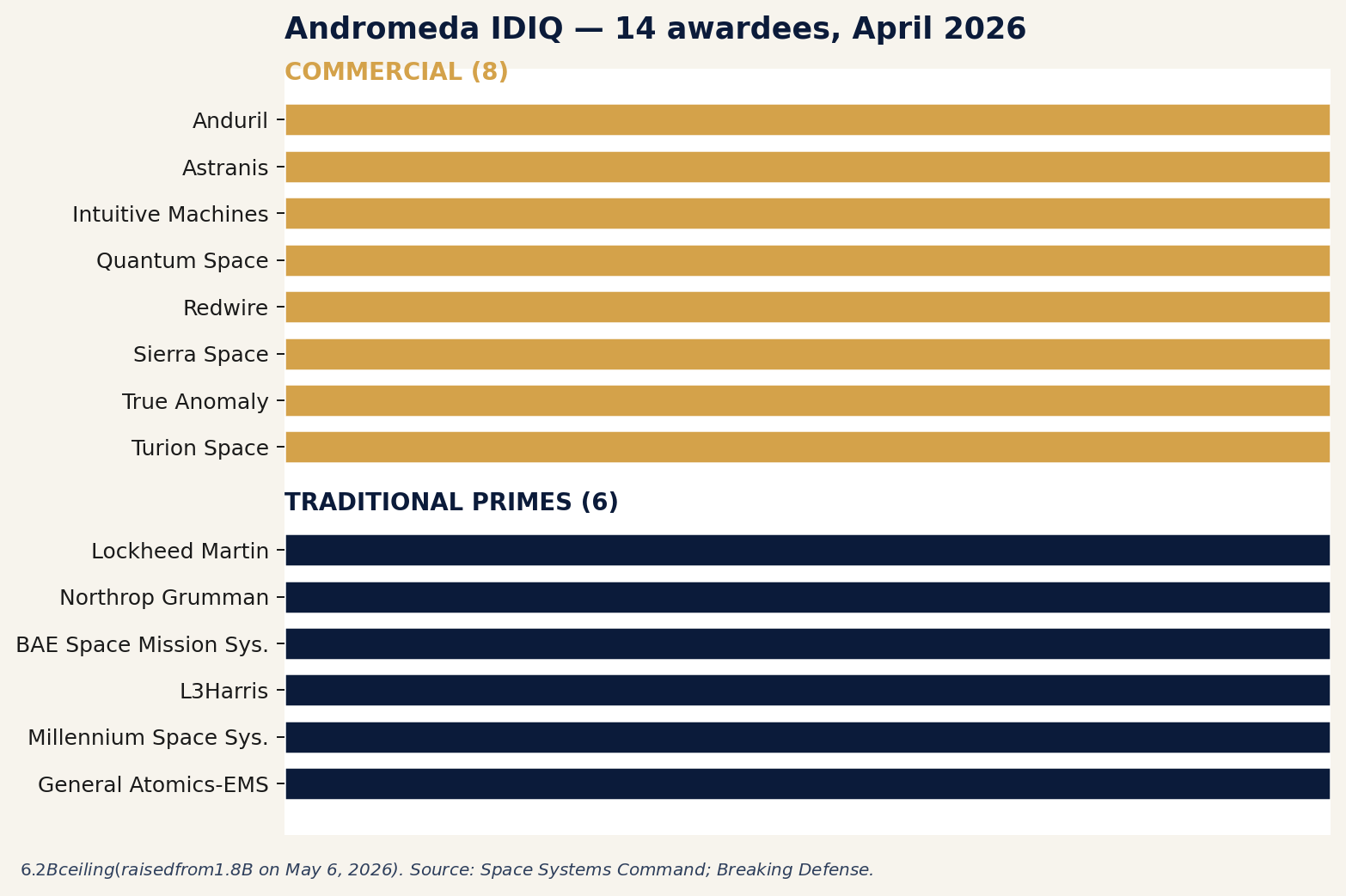

Two weeks before the S-1 hit, on May 6, the Space Force made a quieter but equally telling move: it raised the ceiling on the Andromeda IDIQ contract vehicle from roughly $1.8 billion to $6.2 billion — a $4.4 billion increase just weeks after the original award.

The stated reason was blunt: the FY27 budget was “significantly increased” to address “the escalating threat environment projected for CY 2030+,” according to Breaking Defense. Translation: Russia and China are moving faster in GEO than the legacy architecture was sized to handle, and the Space Force is buying its way out of that problem in a hurry.

The constellation that is aging out

For two decades, U.S. national security space has rested on a quiet assumption: we could see enough in geosynchronous orbit to deter, diagnose, and respond. That assumption is getting harder to defend.

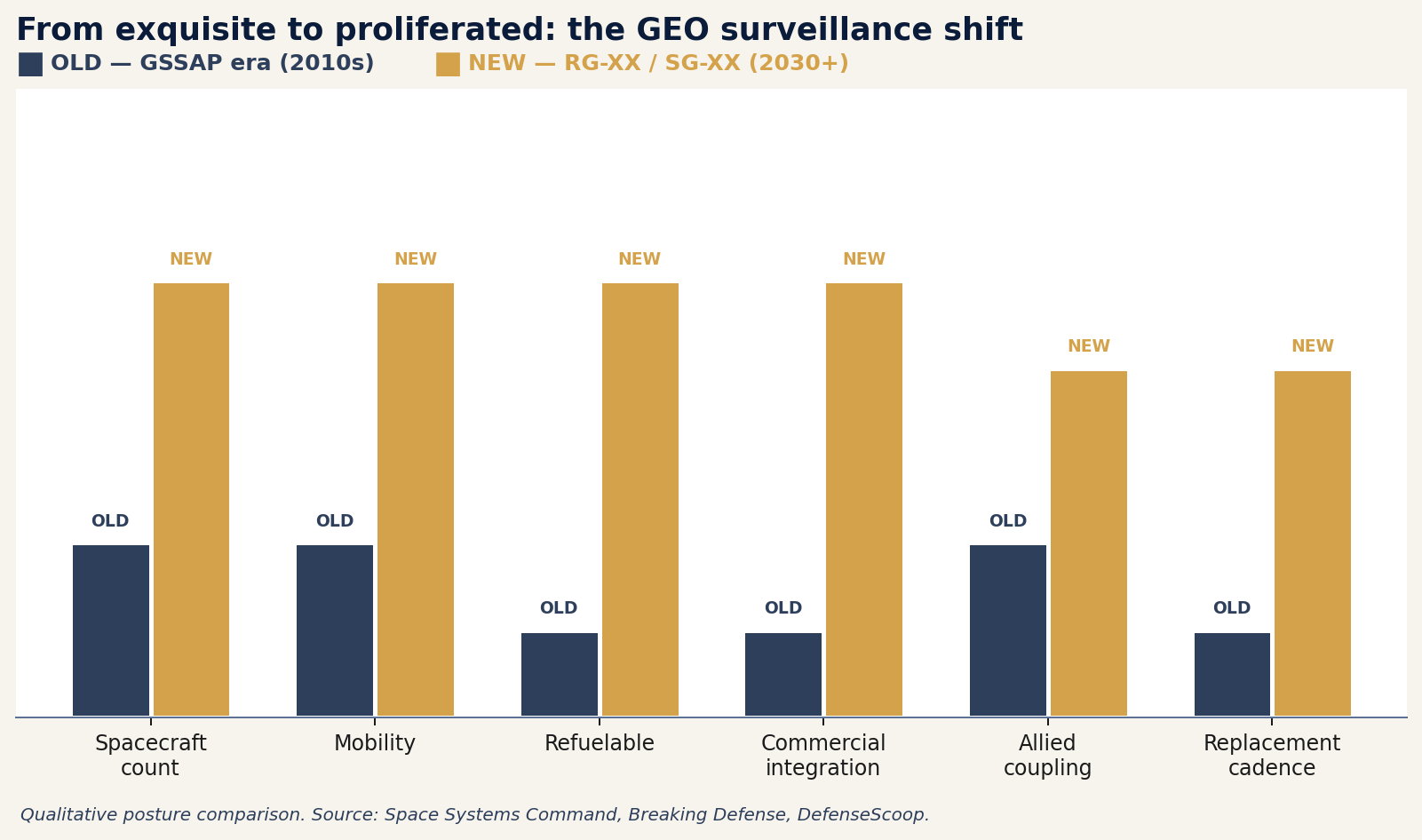

The legacy model was a small number of exquisite spacecraft — most visibly GSSAP, paired with classified systems such as SILENTBARKER and allied sensors. It worked when the threat moved slowly, the targets were relatively few, and the penalty for sparse revisit was manageable.

That world is gone. China’s SJ-21 demonstrated the ability to dock with a defunct satellite and move it to a graveyard orbit — a capability that looks benign in a debris-removal frame and very different in a counterspace frame. Russia’s Luch/Olymp satellites have spent years conducting close approaches around commercial and government spacecraft in GEO. China’s TJS series continues to grow, and the Space Force has become less willing to describe publicly what it believes some of those spacecraft can do.

The U.S. response is now taking shape: RG-XX to replace GSSAP, and SG-XX to replace the SILENTBARKER surveillance layer. Both sit under the Andromeda vehicle.

The shift from a handful of exquisite watchers to a proliferated, refuelable, allied-coupled architecture.

What Andromeda actually is

Space Systems Command awarded 14 Andromeda IDIQ contracts in April for RG-XX, a program focused on rapidly fielding proliferated space domain awareness capabilities in GEO. The goal: detect, track, and characterize resident space objects of interest, and achieve space superiority at scale in 2030 and beyond.

The awardees are worth reading closely.

The primes are there. The commercial slate is the signal.

The primes are expected. The more interesting signal is the commercial slate. Anduril, Astranis, Quantum Space, Redwire, True Anomaly, Turion, Intuitive Machines, and Sierra Space are not window dressing. They point to an architecture that is smaller, more numerous, more maneuverable, and more commercially derived than the one it replaces.

Breaking Defense described RG-XX as expected to use “smaller, lower-cost commercial satellites with more mobility, a refueling capacity and a longer life span than the GSSAP sats.” DefenseScoop reported last year that Space Force leadership viewed on-orbit refueling as a requirement for RG-XX, not a nice-to-have.

That matters. A refuelable SSA spacecraft is not just a better camera platform. It is a different operational concept. It can hold position longer, revisit more often, maneuver without spending itself into retirement, and create an installed customer base for the in-orbit servicing market the government has been quietly cultivating for years. Watching becomes maneuvering. Maneuvering becomes servicing. Servicing can become denial.

What the $4.4 billion move tells you

A ceiling raise this large, this quickly after award, is unusual. It likely tells us two things. First, the threat picture changed between the FY26 and FY27 budget builds. The “CY 2030+” language is not filler — it is the planning boundary inside which the Space Force appears to believe the GEO surveillance problem becomes materially harder.

Second, the Space Force is creating room to buy at fleet scale. The Space Force requested $355 million in FY27 for RG-XX and $370 million in FY27 to begin SG-XX development, with multi-year totals in the billions for each line. That is a different signal from “replace a few satellites.”

The context most coverage is missing

Three adjacent developments make Andromeda look less like a contracting story and more like a strategy story.

Allied SSA integration is becoming operational. U.S. Space Command conducted a second bilateral space domain awareness operation with France under Multinational Force Operation Olympic Defender — France described it as the first operation conducted within the Olympic Defender multinational framework.

The communications layer is moving. DARPA is winding down Space-BACN, and its optical inter-satellite link work is transitioning to DIU for future demonstration. A proliferated GEO surveillance layer becomes far more useful if it can share data across space links rather than always routing through the ground.

The servicing ecosystem is maturing on the same clock. Rocket Lab announced a definitive agreement to acquire Motiv Space Systems on May 7, adding Mars-proven robotics, motion-control systems, and precision mechanisms to its vertically integrated space systems business. That is not GEO refueling, but it is part of the same industrial base: precision mechanisms, proximity operations, servicing, manipulation.

These lines are converging. The future GEO surveillance architecture is not just cameras in orbit. It is maneuvering spacecraft, crosslinked data, allied operations, refueling interfaces, and eventually servicing-grade hardware.

The Common Thread

Read these two announcements together and a pattern emerges that neither story tells on its own.

The commercial side is collapsing into one vertically integrated stack — launch, broadband, mobile, AI compute, classified constellations — backed by a single balance sheet and a single decision-maker. The national security side is moving the opposite direction: away from a handful of exquisite spacecraft and toward a proliferated, mixed-vendor, allied-coupled architecture that explicitly assumes the commercial industrial base is part of the answer.

Those two trajectories meet in the same place. SpaceX’s Starshield is on the government side of that intersection. So is Anduril. So is Astranis on Andromeda. So is Rocket Lab buying Motiv. The line between “commercial space company” and “national security space supplier” is functionally gone for the companies that matter.

This is the moment the space industry stops being able to pretend it operates inside its own little ecosystem. The capital, the spectrum, the AI compute, and the surveillance architecture are now one conversation.

What to Watch Next

· June 4 SpaceX road show, June 11–12 pricing. Watch whether the offering prices above the $1.75T anchor or above $2T. The premium sets the valuation ceiling for every other space IPO for years.

· Telco response. Look for AT&T and Verizon to push back on FCC equivalency standards and accelerate their own AST SpaceMobile commitments. Expect at least one merger conversation to leak.

· First Andromeda task orders. Ceiling increases are intent; task orders are commitment. Which companies receive the first RG-XX prototype and production orders will reveal what architecture the Space Force actually wants.

· The SG-XX vendor mix. If awards consolidate around traditional primes, that tells one story. If commercial vendors penetrate SG-XX too, the proliferation thesis is now official doctrine.

· Allied coupling. France, the U.K., Japan, Australia, and Germany are moving toward architecture-level coupling — common tasking, shared custody, combined operations. The next milestone is operational, not declarative.

· Refueling. “Refueling capacity” is the most underweighted phrase in the Andromeda coverage. If RG-XX really bakes it in, the Space Force has just created a real anchor customer for the in-orbit refueling market.

· Competitor financings. Pressure on Amazon Kuiper, OneWeb-Eutelsat, and China’s Guowang to demonstrate capital and cadence spikes the moment SPCX starts trading.

The Bottom Line

The S-1 is the moment the commercial space industry stopped pretending the rocket was the product. Andromeda is the moment U.S. national security space stopped pretending a small number of exquisite watchers could hold the high frontier.

Both moves were predictable. Neither moved the needle when they were predictions. Both have now moved from forecast to filing — one to the SEC, one to the federal contract registry. The competitive map of this industry has been redrawn in fifteen days.

The launch business will keep flying. The interesting questions are now upstream of it.

Thanks for reading. Share this with someone who should be paying attention.